A Homeowner's Nightmare: How the Collapse in CRE Value Is Sparking a Municipal Tax Crisis

An empty skyscraper downtown means rocketing taxes at home.

Hi! My name is Ralph Saint-Franc, also known as sirralphie2k on X/Twitter, and for months on X/Twitter I have been warning about the one thing that’s going to make everything worse on the local level: rising property taxes due to falling values of commercial real estate. Everyone wonders: “if the values of office buildings drop, does that mean lower taxes for us?”

The answer to that question is a resounding HELL no.

In fact, it raises residential property taxes for everyone!

For many decades, commercial property taxes has been the number one source for tax revenue for many cities across America, being at rate that is double or quadruple of your home’s value. With the tax revenue drying up, it means that it’ll have to raise other taxes including residential property taxes.

Let’s break it all down so that you can understand.

Where Cities Across America Get Their Revenue (And How Overnight It is Disappearing)

According to the Tax Foundation 56% of the property tax revenue on average for cities comes from commercial and industrial properties. Here’s the craziest part: they are a much smaller slice of the total real estate! This leaves with 44% of the property tax revenue on average coming from homeowners. That means that cities are heavily banking on commercial properties to fund their services such as firefighters, schools, policemen, parks, libraries, mailboxes, and finally healthcare for city workers. Talk about putting your eggs in one basket! So to translate, your tax was kept artificially low due to the amount of commercial tax revenue cities were getting.

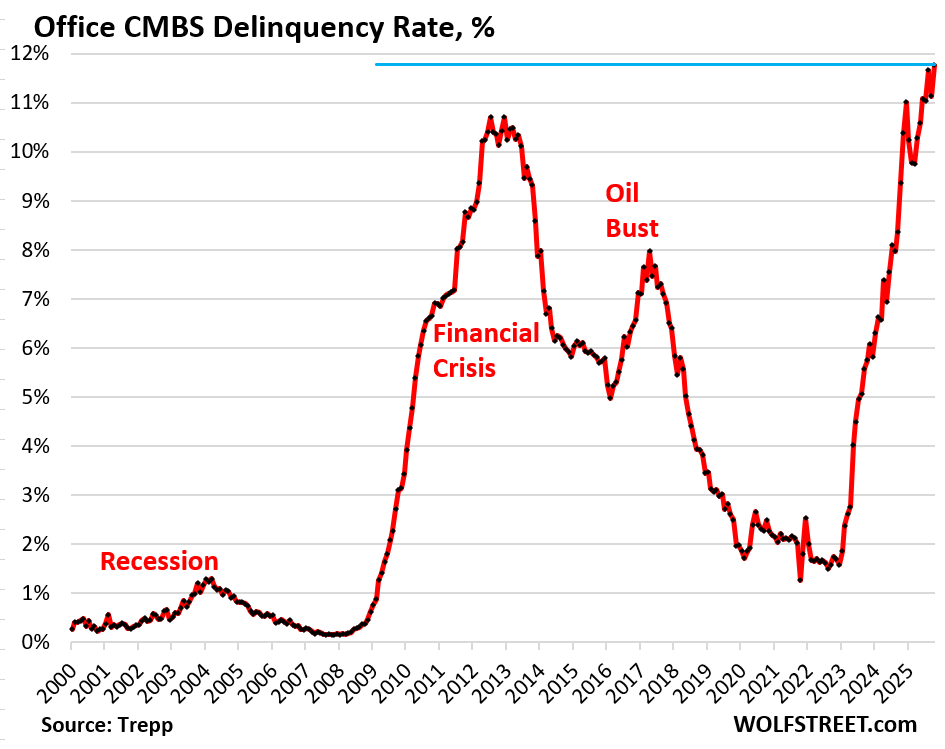

Today, in the latest report from Wolf Street in November, Office CRE delinquencies has soared to levels not seen…. EVER, sitting at a horrifying 11.8%!

For those that may not know, being delinquent means you either failed to make a loan payment 30 consecutive days past the due date OR you failed to make a payment on your maturity date (The final day of the loan being paid)

Now what happens when someone is delinquent on their Office loan? Well here’s a step by step:

1. The bank takes the keys away.

Now the building legally belongs to the bank.

2. The bank has to sell the building quickly.

Banks hate owning an empty building, so, they put the building up in an auction or they put it under a fire sale.

3. It sells for pennies on the dollar

The $100 million now sells for anywhere between $30-40 million. That’s 60 to 70 cents on the dollar or 60-70% discount. That means the market value of the building was slashed by 60 to 70%. OUCH.

4. The tax assessor then sees the sale (this is the person that asses the value of the a building in a municipal area).

The tax assessor pays attention to the value of the building that was sold last month, not last year or even 5 years ago. So the assess value gets slashed from $100 million to $35 million overnight.

5. Down goes millions in tax revenue immediately.

If that particular building was paying anywhere between $2-3 million in property taxes, now it pays $600k-$900k. So who pays the $1.4-2.1 million difference? It’s you and every homeowner that is living in your town.

They love to say one man’s loss is another man’s gain, but it turns out when it comes to CRE, the one man’s loss is the twenty thousand homeowners that saw a big tax bill.

The Warning Shot That Was Fired Months Ago Are No Longer Warnings

Well, this is where people like to say: I got receipts!

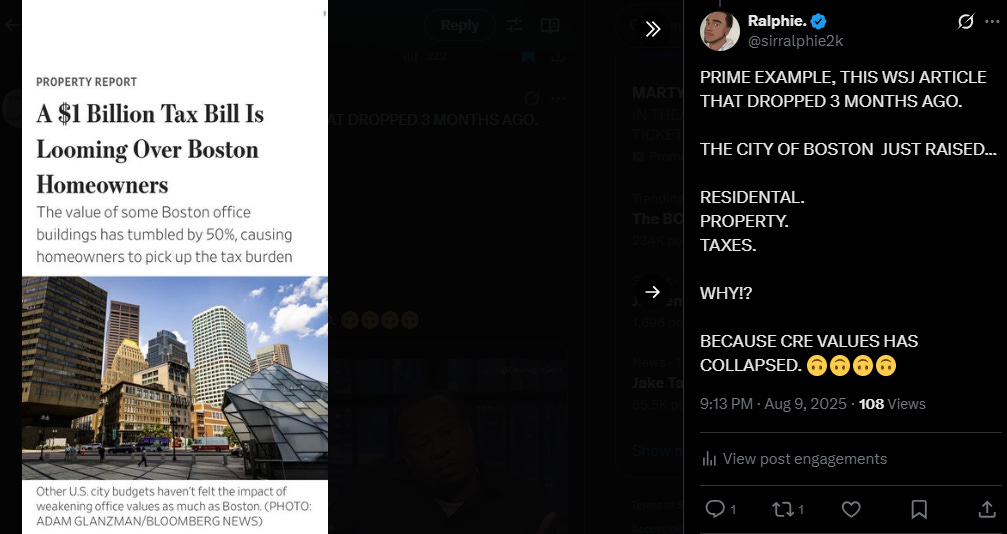

In this thread from August 9th, I said that to offset the loss of tax revenue, local governments will have to raise property taxes. A Wall Street Journal from May 5th had a bombshell report where homeowners in Boston is facing a billion dollar tax bill due to some building seeing values dropping 50%.

But that isn’t the ONLY city that is facing distress, there’s cities like Seattle, Chicago and Minneapolis are all facing the same pressures!

Do you, the reader, honestly think it stops in those cities? Nope it doesn’t because cities like Portland, New York, Philadelphia, Miami, DC, Providence, Houston, Dallas, San Antonio and much more are all going to be facing those types of pressures. To make things worse, cities aren’t the only entities feeling the heat.

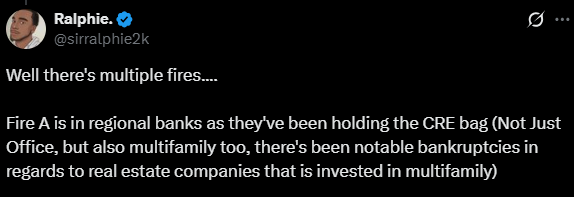

It’s Not Just a Municipal Thing—It’s Also a Regional Bank Thing

This entire fiasco doesn’t stop at municipalities unfortunately. Remember earlier in the step-by-step process the banks takes they key? I didn’t specify witch type of bank up until now, and that type of bank is….

Regional Banks.

In a Setptember 2025 research paper from the University of Pennsylvania, researchers found that a third of the $4.8 trillion in CRE debt is held by regional banks, along with holding a majority of all non-owner-occupied commercial properties. The same research paper found that hidden distress in regional bank portfolios is estimated to be 4 times higher than what the official delinquency numbers are showing.

To make matters worse, banks overall in 2026 will see over $1 trillion in CRE debt maturing and who holds the significant share of it? Regional lenders! Furthermore, according to Reuters, 20% of the maturing loans this year has all been from Office CRE, and this is the hardest hit sector all year.

In plain English, it means that these regional banks over the next 2 years are going to have to a massive amount of provisions (money set aside for potential loan defaults), and that means they’re will have to seize the non-preforming buildings, put them on a fire sale which means more tax revenue loses for cities, which means an even bigger tax hike for your house.

Here’s the scariest part: This isn’t coming, it’s already here, and it’s about to get much… MUCH worse.

This piece was very insightful with a tone of valuable information. Thank you for sharing!!