Bond Yields Go South of Heaven When Deflation Is Present

When there's rate cuts, people cheer. Few realize it's a sign that the economy is dead.

When you sit on your butt, wither it is scrolling on social media, or you’re watching television, you see the news from mainstream media, and personalities: “The Fed cuts 25 basis points — here’s what this means for you”

Then you have reactions like

“This is wonderful news for Americans, it will make things more affordable!”

“This is amazing news, we beat inflation!”

“This will make people buy homes!”

All I got to say is this: THEY ARE ALL WRONG!

Now, the biggest needle mover of any market is the Bond Market! This is where banks, both commercial and central, institutional traders, and yes, even governments, no matter on what level are at, as it is the largest market in the world! Now before we really talk about the bond market, we need to first establish a view key points about bonds in general…

A Bonding 101 Moment….. But Not In a Way You Think!

A bond is where you lend money to either a government entity (doesn’t matter on what level) OR a corporation.

The component of the bond, is just like the loan, there’s 3 parts:

- The Principal (the amount you lend)

- The Interest Rate (this is where instead of you paying interest, you EARN interest)

-The maturity date (the date when you get your money back)

Bonds, like stocks, are traded every single day. There’s 2 things that always changes: The bond price and bond yield.

The bond price is what you pay for the bond today, The bond yield is what you would earn if you were to buy the bond today.

The yield formula is simple:

Yield = The Annual Interest payment (The payment given to you from a government or corporate entity) / The current price of the bond

Okay time to run an example:

Let’s say the US Treasury issues a new bond that costs $1,000 and they will pay you $50 a year, and the bond expires in 10 years. So, when you do the math, you get a 5% yield, not too bad!

Now, let’s say somebody brought the bond for $1,500, because they’re panicking and they don’t trust anyone. Now the problem is, the bond they brought only pays $50 a year. So when you do the math…. The yield went from 5% to 3.3%.

Would you look at that, you know bonding better than some couples all around the world! Call me a relationship expert, because I solved your relationship problem with bonds!

What the Bond market Is Truly Saying

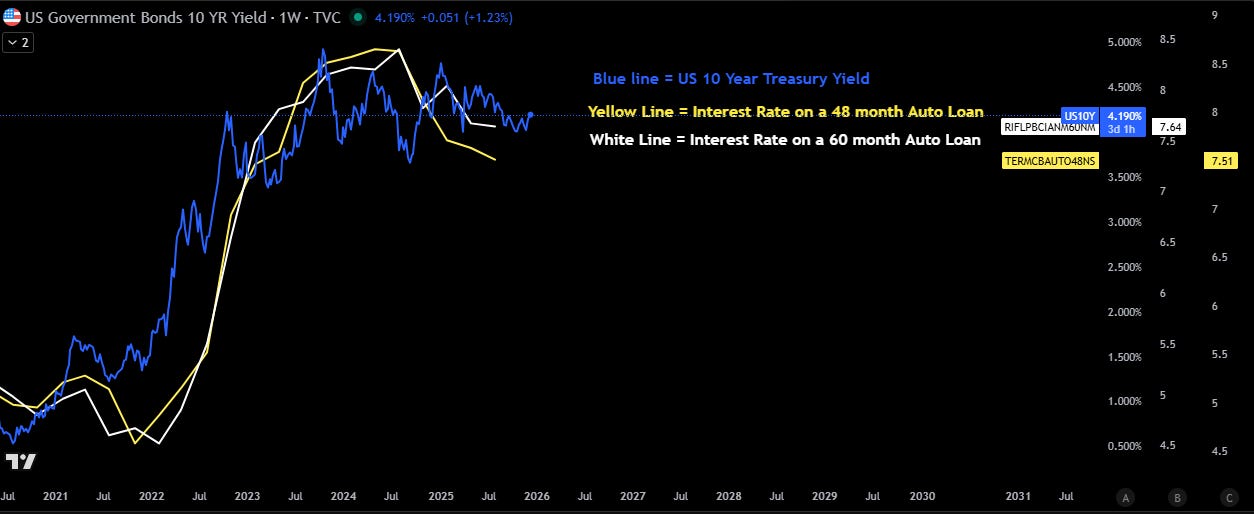

Okay, so the investors, institutional traders all follow the US 10 year treasury. Why?

Well of 2 things:

A. Your mortgage rate, as well as your auto rate, follows the 10 year treasury almost to a T!

B. The 10 year treasury yield serves as growth and inflation expectations.

This means the traders prices in growth and inflation expectations over the next 10 years.

A higher 10 year yield means there’s going to be growth and inflation, by growth, I mean CREDIT GROWTH, and the outlook on credit growth is absolutely DOGSHIT.

In my last article, I mentioned about how consumers has been delinquent in their auto loans, credit cards and student loans.

And guess what? Being delinquent means banks won’t lend to you, because they don’t trust that you can pay the loan back!

What happens if 50 million people are delinquent on their loans!? The economy DIES. Why!?

Banks lending less means there’s less money in the system, meaning that money moves slow which leads to asset prices as well as prices of everyday goods and services going down. THAT’S DEFLATION!

So if credit growth collapses, that means inflation expectations significantly decrease, which will lead to a panic buying bonds because banks are not willing to lend money out to people that are delinquent!

But what about globally? Is it looking good?

To quote the famous Randy Jackson:

IT’S A NO FOR ME DAWG.

Globally, Everyone is flocking to Safety Part 1: The Land of The Rising Sun Full of Debt

We need to go West in the Pacific Ocean, to a land that always seeing a rising sun: JAPAN!

Let’s take a look at their 10 year yield……

Yields are BLOWING out in Japan, what the hell is going on?!

We need to talk about Debt-to-GDP (Gross Domestic Product) Ratio.

Firstly, Gross Domestic Product is the total value of goods and services that was produced within a timeframe, wither it is a quarterly or yearly.

Now Debt to GDP is comparing a government’s national debt to its GDP, showing their ability of paying their money back, express as a percentage. A High Debt-to GDP ratio means a country is at high risk of declining their economic growth and potentially default on their current debt.

Now according to World population Review, Japan’s Debt to GDP is….

DRUMROLL PLEASE….

255%!!

How?

Well, Japan back in 1980’s had a stock market and real estate bubble as people borrowed hella cheap money and speculated on them. Now in 1991, the bubble burst and the growth collapsed to near zero, that caused as many calls it, The Lost Decade, and ever since then, Japan never recovered!

Why?

Because the government borrowed money like a person on crack just to stimulate the economy, and their GDP barely moved, all the while the BOJ has been artificially keeping rates low by buying every bond in their sight. This is called Yield Curve Control, and the goal is to make sure the yields don’t go bananas.

But now that they let the yields rise just a tiny bit, their bond market has been screaming on top of their longs for all kinds of help. So what has the BOJ done? They print a shit ton of yen just to buy the bonds to calm them down which causes the value of the yen to weaken.

As a bonus, Japan just pass a stimulus package to stimulate their economy last month! Things will end well…. right? RIGHT!? Wait, why do I hear Mount Fuji erupting…..

WELP TIME TO MOVE ON TO EUROPE BEFORE I GET CAUGHT IN THE FINANCIAL VOLCANO!

Globally, Everyone is flocking to Safety Part 2: The Return of a European Debt Crisis

A Return? Yeah! We need to rewind the clock back to 2010, where the original European Debt Crisis happened…

This story took place in the PIIGS countries (Portugal, Italy, Ireland, Greece and Spain) these countries along with the rest of the countries was united under one currency: THE EURO!

Before the GFC in 2008, The 2000’s in Europe was full of countries borrowing money with low interest rates, and economies in those countries was doing pretty well, and the banks in Europe was more than happy to lend to a booming union!

One day in late 2009, Greece broke the news to the union: “Uh you know how we

have borrowed billions to spend in our economy? Turns out the real amount is way more than we thought, and we actually may not have the funds to pay our debt back.”

Within months after the announcement, Greece’s 10 year yield went from about 5% and went at high as almost 40% within a span of a year in a half…

And what happened next, it spread like a raging super wildfire

Ireland’s bank melted down because of all thanks to the real estate crashing (There were banks in Ireland that invested in the US real estate market and their real estate market crashed in 2008, but there was some who had invested real estate at home at the time of the European Debt Crisis)

Portugal also had too much debt like Greece, and like Japan, they too had weak growth..

Spain was in the same situation with Ireland…

Finally, Italy was in a political grid like as debt was raining down on them like a waterfall.

Their respective 10 year yields went coco for bananas, meaning there was no demand for their bonds meaning Bond Prices CRASHES.

And as PIIGS was getting cooked harder than Brazil against Germany in the world cup back in 2014, there was some severe fallouts that came:

The Euro Stocks Crashed, High levels of unemployment all across Europe, and there was banks in Europe that were becoming insolvent since they were holding the junky bag of bonds.

So who saved the day like a good little superhero?

The European Central Bank, The International Money Fund, and Finally Rich European countries like France, UK and Germany. ECB brought a large amount of bonds (This is called Quantitative Easing), IMF wanted countries to implement Austerity measures (Such as Tax hikes as well as cutting spending). The total amount that pumped into the European Financial System: Over €700 billion!

After the yields finally stop going coco for coco puffs, the damage was done: There is slower growth, even more debt being piled up, and a growing recement towards governments by Europeans.

Today in 2025 here’s the latest Debt to GDP Numbers (From Highest To Lowest) according to World Population Review in the PIIGS countries:

Greece: 162% of GDP

Italy: 135% of GDP

Spain: 108% of GDP

Portugal: 99.1% of GDP

Ireland: 43.7% of GDP

France, who was involved in the bailout process now has a Debt to GDP ratio of 111% While England is sitting at 97.6% and Germany at 62.9%.

Thanks to the ongoing Ukraine war, there has been Energy Shocks, there’s been continuing slow growth, and inflation has never hit ECB’s goal.

The ECB all of last year, and the first half of the year has been cutting rates to stimulate the European economy, and despite that, yields are still rising in some weak European countries as investors are literally afraid of getting the junk bond touch. So what will ECB have to do again? Yep….. they’re gonna have to buy those bonds at a LARGE amount… again! But this time around, will they have enough ammo? Only time will tell….

When a Land of the Rising Sun, And the Europeans Can’t Pay Their Bonds, You Run to the Land of the Free As a Safety Flight

At the end of the day, if Europeans can’t pay their current debt, if Japan can’t pay their current debt, where’s the only place that investors are gonna go that is the most liquid?

The US Bond Market.

The US is a global reserve currency, ever since the end of World War 2.

The investors will be panic buying the bonds, driving the yields down and Bond Prices up.

That isn’t a sign of inflation, it’s a sign of deflation.

And to avoid deflations what have countries have been doing?

STIMULUS. PACKAGES.

All you got to do is ask China, ask Japan, ask the US, and ask Europe.

They are all trying to avoid the globe from going into DEFLATION.

But at what cost? The answer is obvious:

YOUR COST OF LIVING.