The Baby Bust Will Bankrupt Nations: The Economic Catastrophe No One's Preparing For

This silent crisis will catch many off guard...

In every healthy society, there’s a simple system that runs on a daily basis:

Babies are born — families get bigger homes— the children fills public schools — young adults take student loans with the parents being co-signers, going to college — the graduates enter the workforce and becomes a contributing member of society, some goes on to become business owners, developers, you name it!

This simple pipeline funds 4 major things:

Real Estate

Municipal budgets

the entire higher-educational industrial complex

Economic growth and corporations

This belt has been working for generation after generation. Today, that belt has coming down into a screeching halt.

How come? Single young men and women as well as young families are being drowned in debt, getting destroyed with household cost rising, and all thanks to soaring cost of living, people has been simply priced out of parenthood.

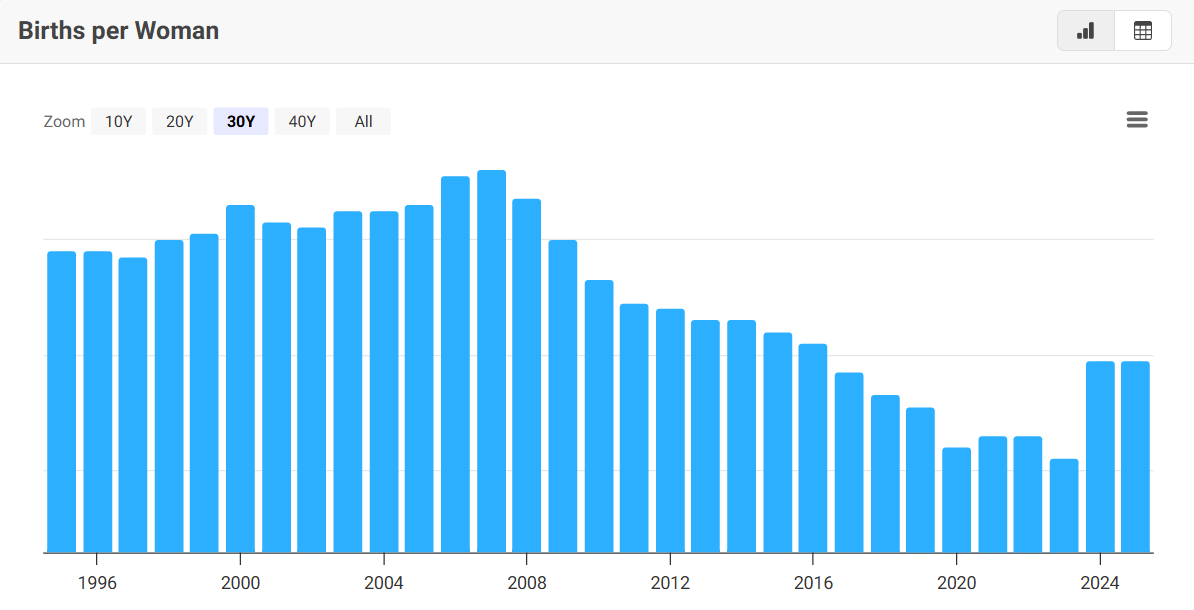

Ever since 2008 in the US, the birth rate significantly declined, including in 2024 where it has made all time lows.

Governments on all 3 levels: federal, state and local governments with their reckless fiscal policy and corporations who has resorted to financial engineering to keep making profits has just made birthing a liability in people’s balance sheets.

The result is quite simple: Birth rates are collapsing, not just here in the US, but in Europe, in Japan, hell, Even China!

If there’s no families that is going to buy houses, no students to fill in classrooms in public schools and borrow money just to enroll in college, and there’s no workers to hire and tax, what happens?

Well, the answer is quite simple: The country faces an existential crisis and the worst part is that this isn’t even a distant problem:

It’s already here.

Chapter 1: The Real Estate Decline

What is the number 1 reason that a young couple buys single-family home?

To start a family.

It really is that simple.

Today, the basic life step has now become a financially impossible for millions of people.

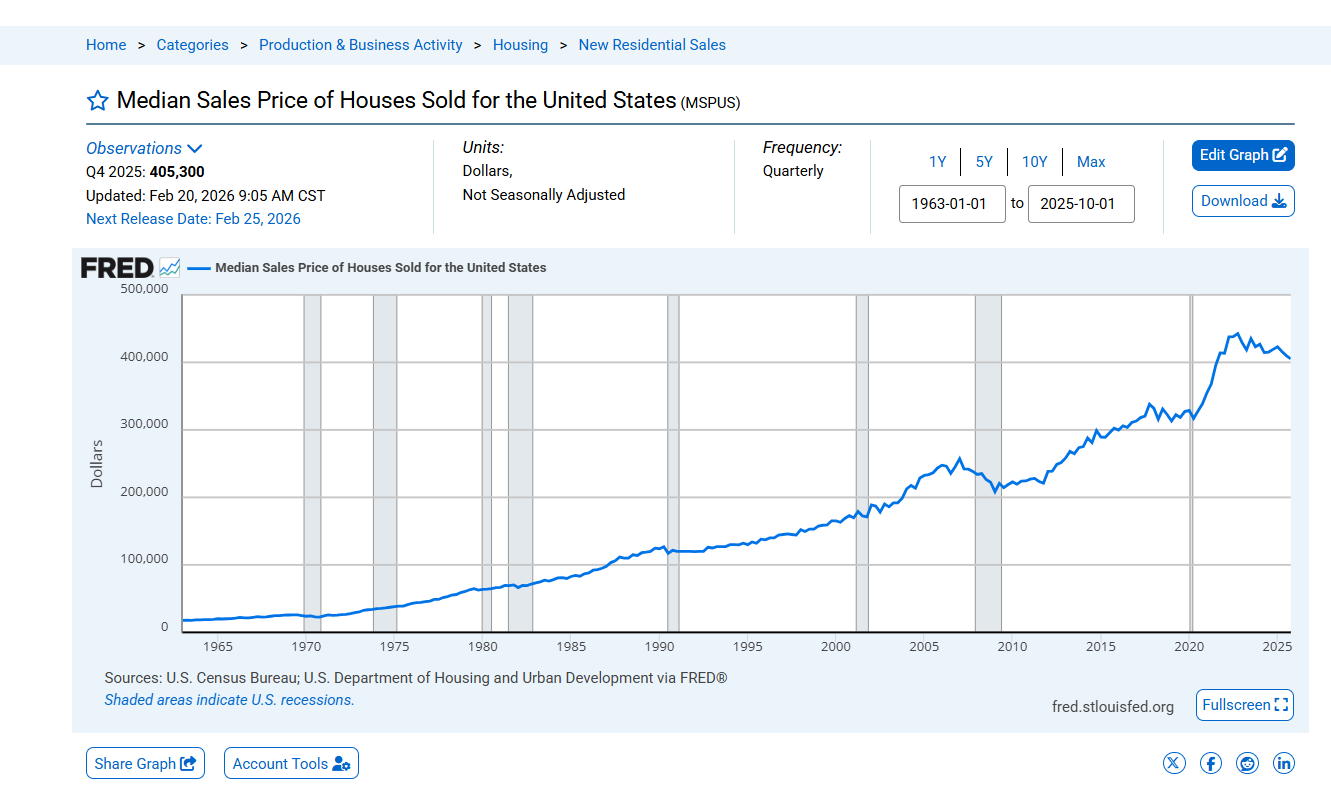

During the global financial crisis in 2008 and then again between 2020 to 2022, the Federal Reserve brought massive amounts of long dated bonds (This practice is known as quantitative easing) that caused yields to go down. and as a result, massive liquidity is now in the system, meaning people can use the money in the system to purchase assets and included in the assets is real estate.

Thanks to the temporary suspension of credit reporting, and massive stimulus payments from the federal government during covid, this has fueled historical speculation in real estate from 2020 all the way to 2022 with the result shown in the data below:

Young families, already facing auto and student loan burdens, is priced out, and the prices exploded so much, it has outpaced wages by a wide margin.

When the credit reporting has resumed, along with a huge wave of inflation due to money velocity (The rate at which money changes hands) increasing, the pain compounded: huge soar in home insurance, utilities and healthcare costs. Add that on top of the minimum payments that they have been making, and what you get is costs that is so high, the young families can not even afford to make babies.

Young families aren’t just delaying home purchases, many have flat out given up on having children all together, which results in even fewer buyers for homes.

As a result, real estate faces a double whammy:

- Buyers refusing to pay for the inflated prices

- Sellers who were chasing the boom find themselves underwater in equity or massive losses.

To make matters worse, the ongoing commercial real estate collapse (documented here on The Market Sentinel) has caused revenues of municipal governments to take massive hits.

With the values of office, multifamily and retail properties collapsing, counties and cities passes the burden to single-family homeowners through sharply higher residential property tax rates.

For renters, it’s a bleaker outlook: landlords passing on rising costs in the form of rent increases.

This movie was played out once in 2008 when the bubble busted from speculation and easy money.

Now, it is the bubble even larger, and the coming demand collapse all due to a decline in birth rates would make what happen in 2008 a joke.

Real estate doesn’t just need lower prices and rates, it needs babies, and today’s home prices are pricing them out of existence.

Chapter 2: The Educational Crisis

Public schools and colleges are built on one simple assumption: a steady stream of children born to young families today.

That assumption is now collapsing.

The timeline is merciless:

In just 5 years, today’s missing babies will leave kindergarten classrooms noticeably emptier.

In 14 years, high schools will run at a fraction of current capacity.

In 18 years, freshman classes in colleges will shrink dramatically.

And today, the decline is already here.

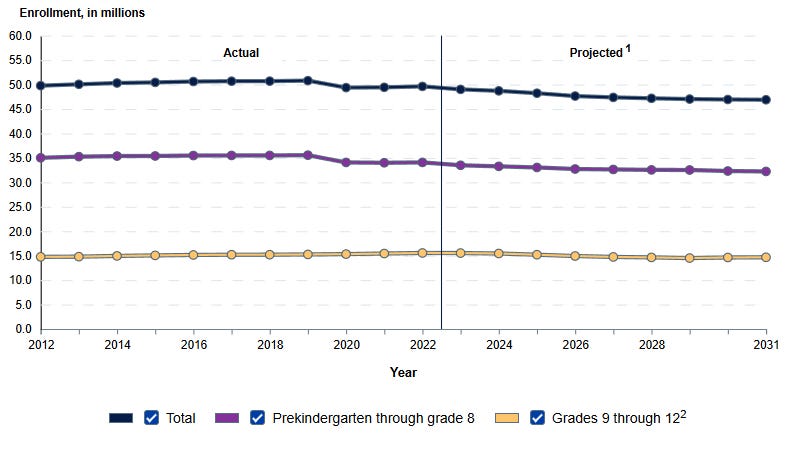

According to the National Center for Education Statistics, as of fall of 2019, national K-12 enrollment peaked at 50.6 million students. In 2023, it dropped by to 49.6 students, and the NCES projects in 2031, 46.9 students would be enrolled.

This is not a small dip — it is the leading edge of a demographic cliff.

Most school funding is tied directly to enrollment (per-pupil formulas). Fixed costs — buildings, administrators, utilities, pensions, and debt — do not disappear when students do. The result is immediate budget pressure on municipalities and school districts.

Hundreds of schools have already closed or merged in states like California, Illinois, New York, and West Virginia. Hundreds more will follow. Struggling districts will be forced to raise property taxes on the remaining homeowners just to keep the lights on — the exact same homeowners already crushed by housing costs.

Public education is often the single largest line item in local government budgets. When that revenue collapses, cities and towns face structural fiscal crises.

But the pain doesn’t just stop there, it intensifies to colleges, both private and public.

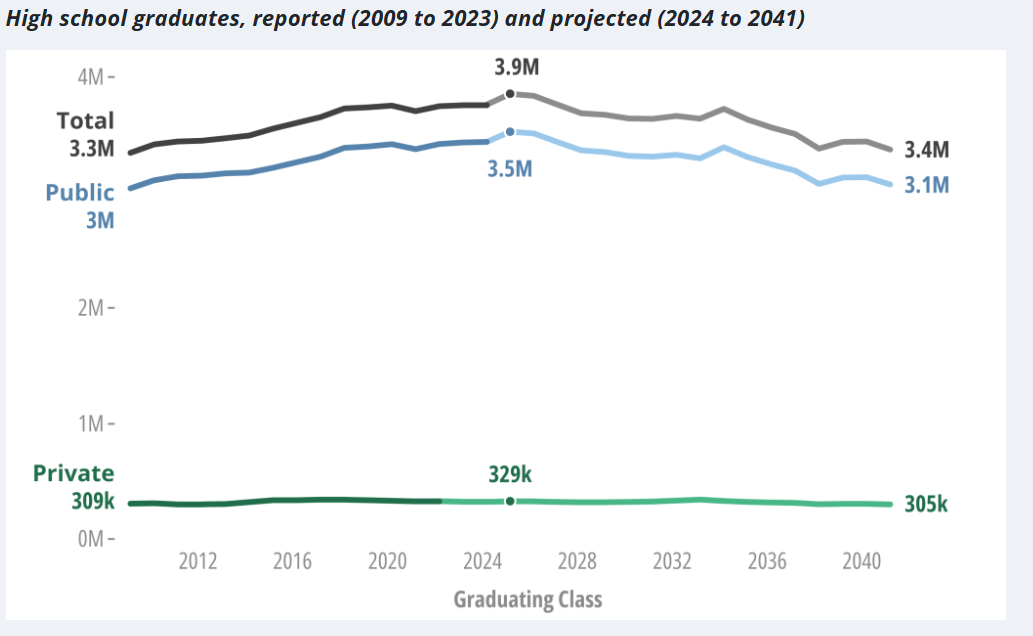

According to the Western Interstate Commission for Higher Education 2024 “Knocking at the College Door” report, the number of high school graduates is set to peak as of 2025 and from there on, that number of high school school graduates it is projected to drop by 13% in 2041.

This “enrollment cliff” will hammer colleges — especially small private schools and regional public universities that depend on tuition revenue. Expect budget shortfalls, faculty layoffs, program cuts, campus consolidations, and a wave of closures.

The education system that was designed for endless growth is now facing long-term contraction — because the babies stopped coming. Empty classrooms and struggling colleges are not just an “education problem.”

They are a municipal finance problem, a local tax problem, and a vicious feedback loop that makes raising children even more expensive.

The systems that once profited from population growth are now being starved by the very fertility collapse they helped create.

Chapter 3: Putting It All Together

You’ve now seen the full picture.

Municipal governments, real estate developers, public schools, colleges, and American companies all run on the same fuel: babies born to young families.

Those systems have spent decades extracting maximum profit from every child — through bigger homes, per-pupil funding, tuition loans, and future workers — while reckless fiscal and monetary policy, exploding student debt, and skyrocketing property taxes have made having those children financially suicidal for most young Americans.

The result? A fertility collapse that is already dismantling the economic foundations these institutions depend on.

Fewer babies today means a shrinking labor force tomorrow. The Congressional Budget Office now projects U.S. labor-force growth will average just 0.5% per year from 2025 to 2035 — almost entirely from immigration. The native-born working-age population is forecast to shrink every single year for the next decade. Companies are already feeling it: slower revenue growth, tighter margins, and chronic labor shortages that no amount of AI or wage hikes can fully fix.

Fewer young families also means slower credit creation. Banks lend to people with rising incomes and growing households. Without them, consumer credit, mortgages, and overall money velocity stagnate — exactly what we’re beginning to see.

Real estate needs buyers. Schools and municipalities need students and taxpayers. Colleges need tuition revenue. Corporations need workers and customers. All four pipelines need one thing above all: babies.

America is no longer producing enough of them.

The consequences — collapsing municipal budgets, crashing home values in family-heavy suburbs, waves of college closures, and a permanently slower-growing economy — are something nobody in power is utterly prepared for.

This isn’t a distant forecast unfortunately, It’s the new reality.

And the those in power will learn in the hardest way possible why this situation should not be ignored one bit.

The link between the birth rate collapse and a potential real estate "demand cliff" is a sobering perspective. Do you think the housing market will be forced into a massive structural "reset" to accommodate these missing generations, or will institutional investors simply keep prices high by shifting us toward a permanent "renter society"?

I’ve subscribed and would be happy to support each other. :)

Jorrit