To be or Not Be Risky: Credit Spreads Tells You If You Should Go Coked Up or Straight To Rehab

When the spread goes high, get your butt to rehab, but when it is low, be in love with the coco!

“HEY JANE! WHERE’S THE COKE!?” yelled Martin, “I found this company that will pay 7%, and I need to get coked up to the max!”

”Martin!” Jane replied, who was cooking dinner for their 2 kids, “How many times do I have to tell you to stop using that freaking coke!? YOU’RE GONNA GET YOURSELF KILLED JUST BY BEING VERY HIGH ON THAT THING!”

You see ladies and gentleman, what happened was quite simple: Martin took a look at the one chart that determines the risk level of the stock market: Credit spreads!

Institutional investors and big money folks looks at this chart very carefully. It tells them if they should be COKED UP (meaning that they leverage debt to trade or invest in stocks) …or go to rehab (As in deleveraging and quickly hiding their cash because they are overexposed AF)

Well, get your notes ready, your popcorn, and maybe your mask ready because it is time to go inside the factory that makes the coke all happen….

Inside The Coke Factory: The Process of Risk Making

Welcome inside! Now, let’s first establish what a credit spread is!

A credit spread is where you take a risky Bond (Ex: Corporate bond, emerging debt market, etc.) and you subtract that from a risk-free bond which is the US treasury bond yield. Now both of these are at the same maturity date. Here’s an example!

We got one worker, Martin here, who lends money to his good buddy, Benny! Benny always pays his bills back on time, and Martin trusts him, so, he charges him a 2% interest.

Now, Martin also lends money to this dude named Eric, Eric doesn’t know when to stop spending money like a drunken idiot, and most of the time he goes broke like a stupid son of a bitch! Knowing this, Martin charges Eric 9% interest. That means Martin would demand that he gets 7% compensation for taking on the risk!

Credit Spreads are basically the extra yield that market demands because they are taking on the risk of companies being hella high on coke, which is basically, borrowing too much money and risking a horrible crash!

Now, those risk are judged by 3 big wardens that are in the factory that determines how coked companies are and they are: Moody’s, S&P and Fitch. These are what the pros pay attention too. Just like school, they grade companies and governments on how likely they are to repay their debt. The better the grade, that means the risks gets to go out for sale, let’s take a look the grading scale from the Big 3!

Tier 1: investment grade. This is an honor roll student! This student has a low chance of defaulting. (This is where Martin’s good buddy Benny is at)

AAA/Aaa = Perfect! Only a very VERY few have earned this grade…

AA/Aa = Beautiful

A = Good

BBB/Baa = Barely made it to the honor student, but their grade still looks good

Tier 2: high yield or Junk. This is the student who has a high chance at failing to repay their loan, but they pay more interest! (This is where Eric is at)

BB/B = Speculative

B = Very Speculative

CCC/Caa and below = BIG TROUBLE ALERT (Default is likely, they’ll have to go to rehab)

D = Already Defaulted

Now, the 3 big wardens uses slight variations of the grading scale. S&P and Fitch uses +/- like A+, Moody’s uses numbers like BB2.

Now that you know what the 3 big wardens and pros are looking at,, keep this in the back of your minds, because now we need to actually go to the part that gets people Hella high on cocaine, and it’s everyone favorite word in the word of finance:

LEVERAGE.

Leverage: The Coke Substance That Makes People Addictive

Ah yes, everyone’s favorite l word after love, leverage! Now, what the hell is leverage?

Basically, leverage is simply borrowing money to really amp up the returns you have. Now it is time to revisit our dear friend, Martin!

Remember how Jane was worried that Martin would kill himself for being very coked up, and Martin found a company that yield 7% in interest? Well time to break it down.

Let’s say Martin had $100,000 on his hand, Martin goes out and buys a B rated corporate bonds that yielded 7%.

Now on the article I did on bond yields, the formula is this:

So, given the yield of 7%, and you have $100,000 to spend, Martin earns $7,000 a year in interest! Not too bad right?

Well here’s the problem…..

Martin wants to get the coke that he desperately needs. He doesn’t want a lousy 7% return! He wants more!

So let’s say he goes to the bank and he borrows $400,000 at a cheap 3% interest rate from the bank.

Now he has $500,000 on his hand that he can use to invest in the same B rate corporate bond yields that generated 7%.

When you do the math, 7% of $500,000 is $35,000 — that’s how much he has earned from the bonds.

Now Martin needs to pay interest on his $400,000 loan, so 3% of $400,000 is $12,000.

Finally, when you take the $35,000 subtract that from $12,000, and you get $23,000. That’s Martin’s net profit on his original $100,000 he had. The yield?!

23%!!!!!

NOW THAT’S THE TYPE OF COKE THAT HE NEEDS!

But is Martin the only degenerate coke head? HELL NO! Do you wanna know who else is a degenerate?

-Hedge funds and Banks, they borrow billions of dollars at cheap rates to buy high-yielding bonds and stocks. Hi Ken Griffin, how are ya today?

-Margin traders that borrow from brokers to buy stocks and options

-Homeowners that puts 20% down on a house, praying that home values go up

-Private equity as the borrow a whole lot to purchase companies and juice returns. Looking you Blackrock…. Vanguard…. yeah all you giant degenerate firms!

Yep, from wall street to your next door neighbor, everyone is HIGH on leverage.

It all works…. until it doesn’t. When it doesn’t work….. financial crises… happen.

The Dark Side of Leveraging: The Causes of Financial Crisis

Now let’s revisit Martin one more time. Remember the 23% yield he gain? Now…. what happens if his 7% bonds loses value?

His $500,000 position would lose 23%, which is a $115,000 loss.

Martin would still owe the Bank $400,000 + interest.

And his original $100,000 becomes -$15,000.

THAT MAN BLEW HIS ACCOUNT.

So now, the bank is going have to call the loan (known as margin call) to force the sale of the bond.

Basically, it confirms Jane’s fear: He killed himself by being too coked up, and now he gotta go to rehab (Filing for bankruptcy).

”MARTIN!!!!! YOU SOLD OUR HOUSE AS COLLATERAL?!?!?!” Jane screamed, then she- OH WHOA WHOA WHOA!!! THAT’S NOT IN THE SCRIPT!! GOT TO MOVE ON! D-DID SHE JUST BROKE A BOTTLE OVER HIS HEAD!? DEAR GOD!

AHHHHHHEEEEMMMM

Okay, now I want you to think about the years, 1929, 1990, 1997, 2000, 2008. What was the common theme in those years?

OVERLEVERAGING.

-1929: People in the US was overleveraged on Stocks and Real Estate. Result? Great Depression.

-1990: People in Japan was overleveraged in stocks in real estate, this was the largest bubble in WORLD history. Result? Caused what is known as the lost decade: Stagnant growth for 10 years, and they have not recovered SINCE.

-1997: Asian Financial Crisis. People were borrowing money cheaply to invest in Thailand and South Korea. Result? Massive Margin Calls that caused a recession in both countries, and the IMF (International Money Fund) had to bail them out.

-2000: People were overleveraged on companies with dot.com on it. Result? Caused a mild recession due to massive margin calls.

-2008: People were overleveraged in Real Estate: Result? A deep, global recession. Massive bailouts for investment banks.

And now today, in 2025, we are seeing it AGAIN, but this time, it is WAY worse: overleverage on stocks, overleverage on real estate (both commercial and residential), overleverage on crypto.

I’ll let y’all figure out how bad this will end, because it is time to talk about the 3 main types of credit spreads pros and the 3 big warders checks out!

The 3 Main Credit Spreads People Watches Over

Now, before we dive in, credit spreads are measure in basis points. 1 basis point is equaled to 0.01%. If the spread blows out, whole lotta people overdosed and they need to go to rehab. If it tightens, people are high on coke. Cool? Alright! let’s dive in! We have:

A. Investment-Grade Corporate Spread. This is a spread for safe companies whose rating that is higher than a BBB, meaning they are the companies that always pays the bills on time!

Now, the symbol for this is BAMLC0A0CM. You can find this in TradingView.

In this picture, the Investment Grade Corporate Spread is sitting at 81 basis points or 0.81%. Now this chart updates between 5 pm and 6 pm after markets close, so if you have time, check it out!

Now here’s the scale you should probably save:

Below 80bp = Calm.

80-150 bps = Normal

150-300 bps = Elevated

> 300 bps = Crisis level

Example: March 18th-20th, 2020. People went into rehab as it the spread went above 300 basis points.

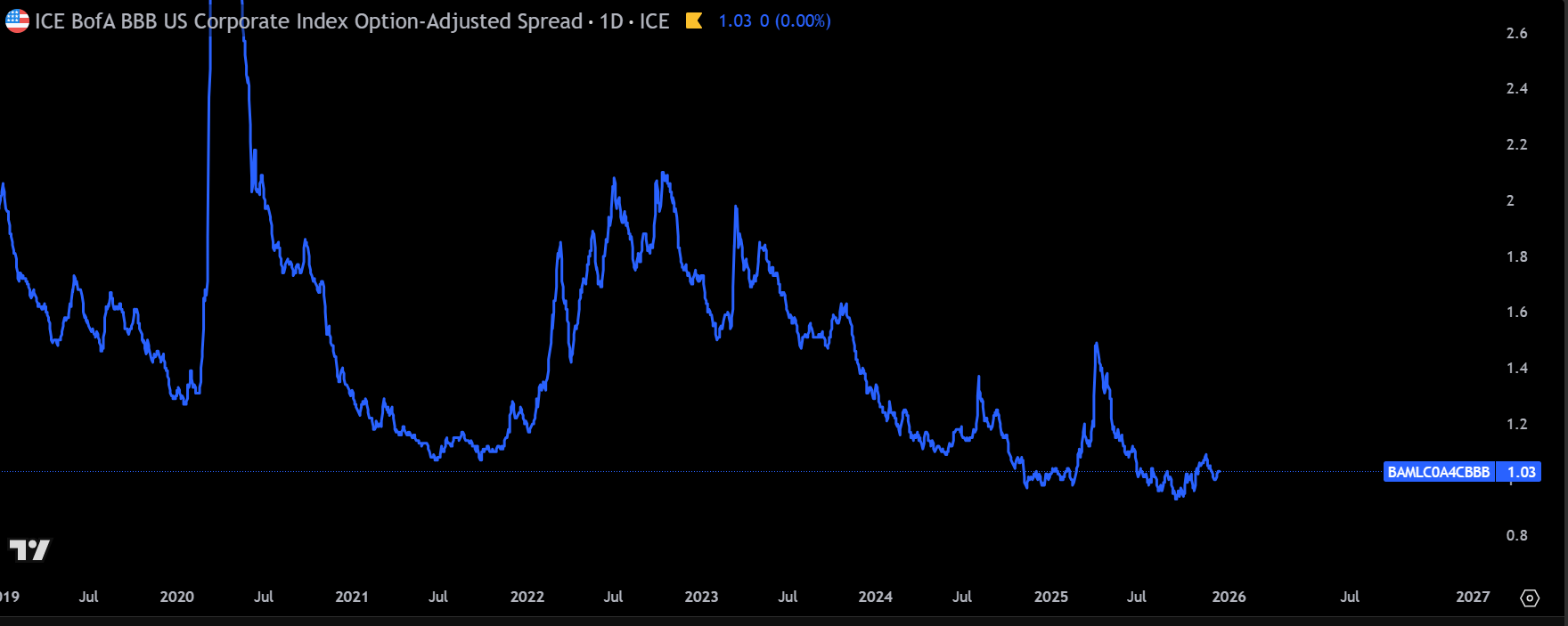

B. BBB Corporate. This is the lowest of the Investment grade, as it focuses on companies on those rated BBB. The symbol for this is BAMLC0A4CBBB and you can also find this on trading view.

Just like the IG corporate, this chart also updates daily, during after market hours here’s the scale to look out for:

Below 150 bps = Calm.

150-250 bps = Normal

250-400 bps = Elevated

> 400 bps = Crisis level

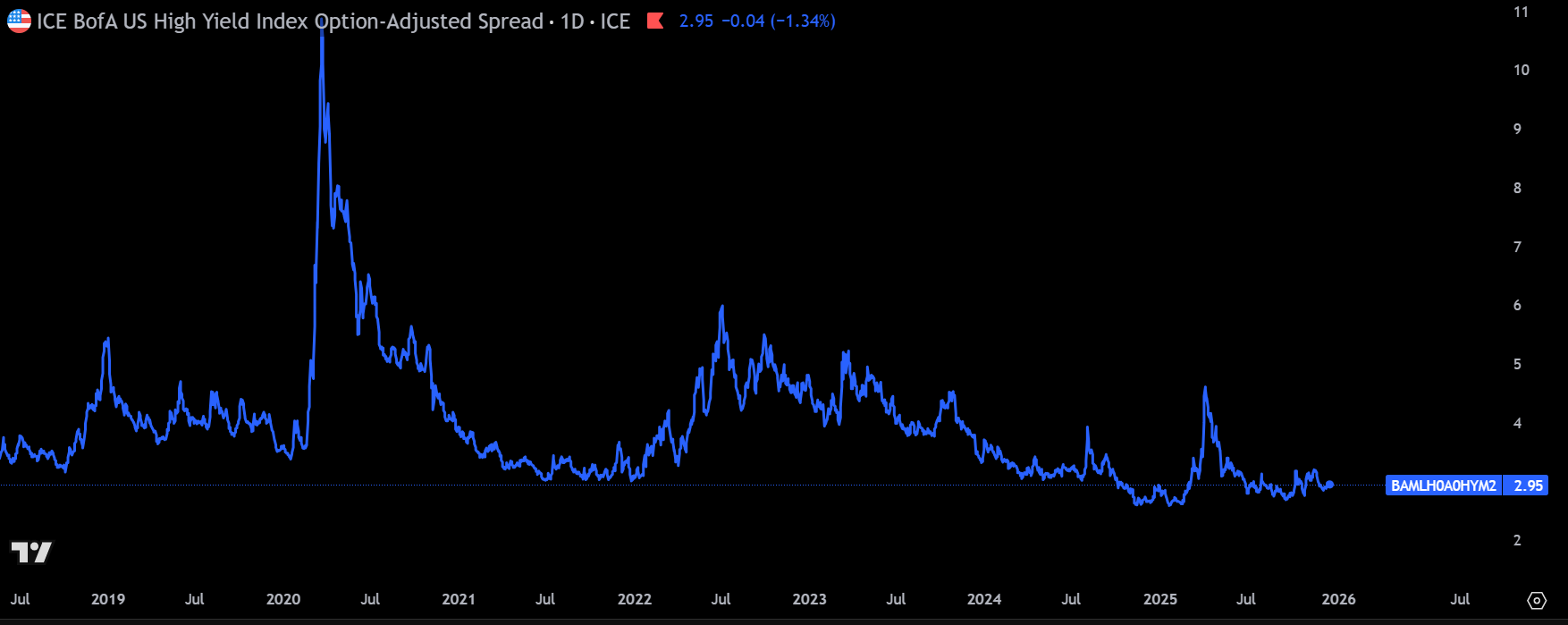

C. High Yield. This is spread for companies that are risker to go into rehab (Rated BB and lower) but they have a higher yield!

The symbol on TradingView is BAMLH0A0HYM2, and just like the other 2 main spreads, this chart also updates daily.

And the scale goes as follows:

Below 300 bps = Calm

300-500 bps = Normal

500 to 800 bps = Elevated

> 800 bps = Crisis mode

Always remember folks, if the spread goes tight, people cokes up in leverage.

If the spread blows out, people goes into rehab.

To be or not be a cokehead is up to you to decide.