Why a Collapse in Credit Growth Is a Sign of Deflation instead of Inflation

Some people have no clue that deflation is the biggest risk in an economy not inflation.

All of you hear it all over mainstream media, hell, even on X: “The dollar’s value is plummeting!” “We’re seeing inflation in prices because due to tariffs!” “CPI is 3% YoY compared to 2.8% last month”

Blah. Blah. Blah. UGH!

What they won’t tell you or you won’t see in headlines on mainstream media though is something that actually matters, and that is Credit Metrics. Delinquencies (People who are 30 days or more late on their loan payment) across every consumer loan class: Auto loans, student loans, credit cards are soaring. Credit rejection rate (This is rate at which people are denied getting loans) are soaring to historically high levels. Those are major red flags.

Now, many of you readers uses a credit card to do an everyday purchase. Credit cards are loans…. and who provides them? THE COMMERCIAL BANKS! And if you don’t pay your loan back to the bank, well, it affects your ability to finance a car, a home, it goes on your record, basically the banks won’t trust that you’ll pay the money back. Now what happens if there’s 50 million Americans facing the exact situation you’re in? Well the banks won’t lend to the economy at all, causing the growth in credit to collapse which leads not to inflation but…

DEFLATION.

Let’s explore why a credit growth collapse is actually bad for everyone involved.

The Money System That Was Hidden From Your Eyes

First things first, we must first establish the Monetary system in place. The United States, along with everyone else around the world has a debt-based monetary system, meaning that in this system, money is created when commercial banks, not central banks, create a loan. The process goes like this:

1. The Bank writes up a loan.

The loan has 4 components:

A. The principal: The amount of money given to YOU the borrower.

B. The Annual Interest Rate: How much you pay in interest on a YEARLY basis.

C. The Maturity Date: This is the day of your final payment

D. Late fee: The fee you got to pay should you be late on any of your loans.

2. You the borrower signs the loan agreement

Now that you agreed to the loan, you have a grace period until your first payment is due. You can use the cash to buy an asset (something that you owe) or whatever.

But what is hidden from you is the main driver behind the entire thing:

THE BALANCE SHEET.

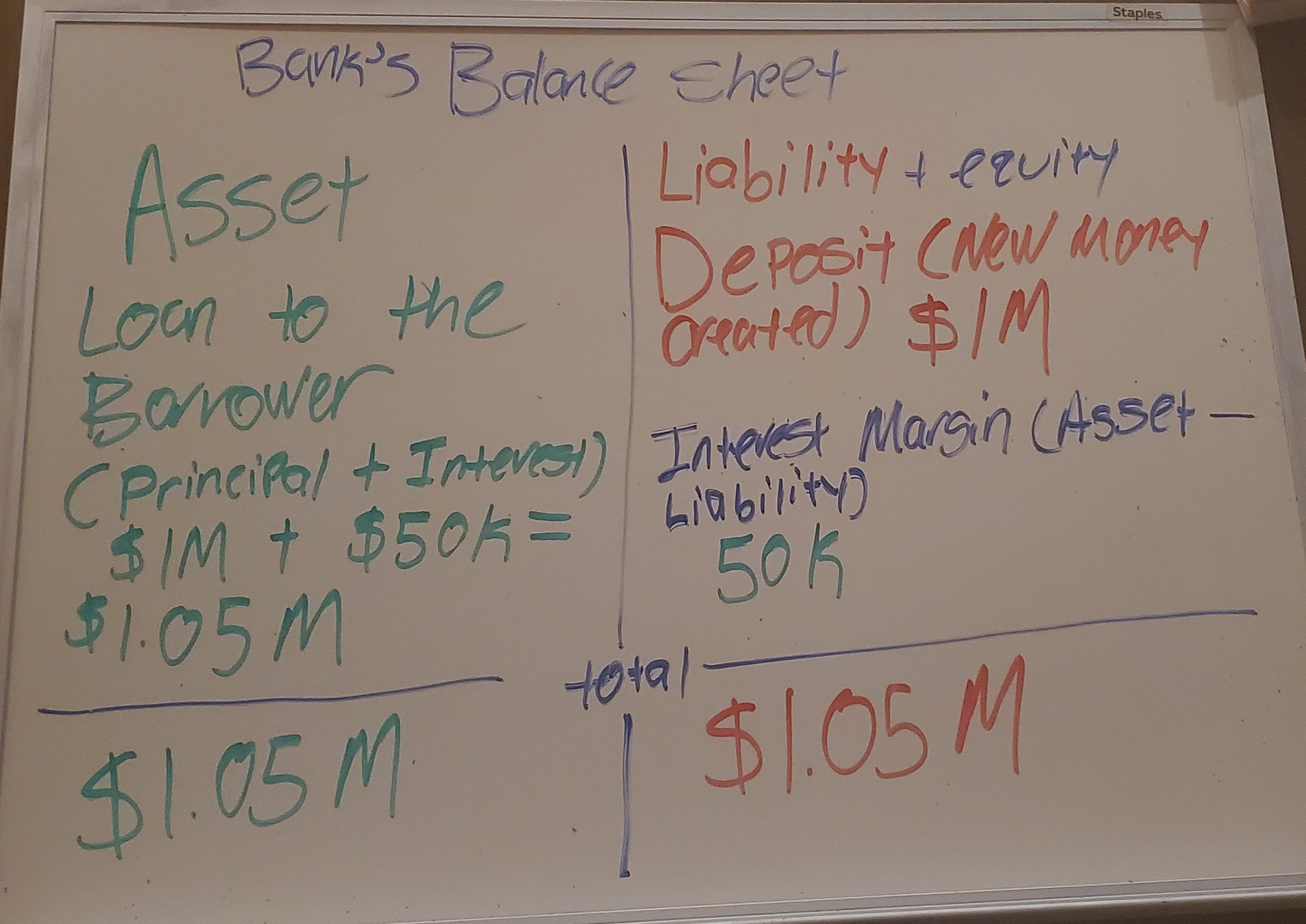

So we have to go in super slow motion beginning with the bank’s balance sheet…

Okay so the bank’s asset is the loan they made to the borrower, why?

Well reader, that’s simply because the bank is has a preforming asset (an asset that generates income) and the borrower is going to repay the loan to the bank.

Now the liability (What you or someone owes) is the deposit they made to the borrower’s account. The deposit is the new money that was created. In plain English, the bank simultaneously created both an asset (the loan) and a liability (depositing the money into the borrower’s account) at the same time. And on top of that, thanks to the principal and INTEREST the borrower has to pay, they get Interest Margin (aka their potential profit through interest receivable). So you basically get the Formula Asset = Liability + Equity, and the sheet balances out. BOOM.

BUT WAIT THERE’S MORE!

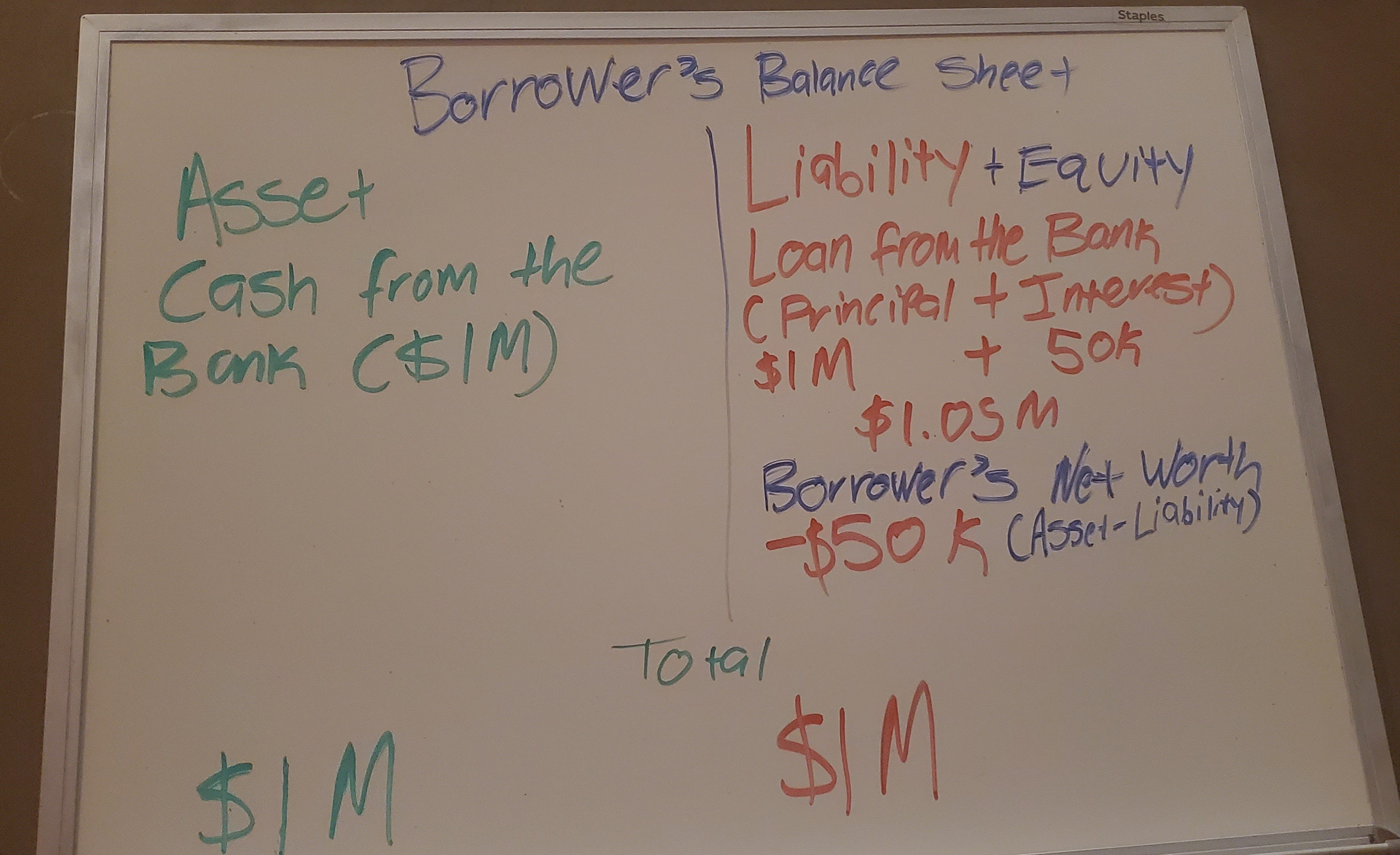

Now we must view the borrower’s balance sheet:

Now for the borrower, they get the the cash from the bank, so that’s an asset, something they own. BUT…. it’s a non-preforming asset because they are SPENDING the money, not EARNING. Cash is NEVER a preforming asset!

The liability they have to is paying the principal back WITH interest.

While on paper, the balance sheet balances out, in reality the borrower owes $1.05 million all thanks to the money being created from thin air.

Congratulations, you have discovered how so many people ends up in a lot of debt!

Now what happens someone doesn’t pay the loan be? Well what the bank is gonna have to write off the loan, let’s say they write off 20% of the loan…. well 20% of $1 million they made the loan is now $800,000, meaning that on paper, the bank is now insolvent, they got 2 choices: Either raise bank capital (Aka their Interest Margin) OR Stop lending so that the balance sheet shrinks back to balance. What does the bank pick? OPTION NUMBER 2! The Prize!? The economy contracting! YA- I mean- BOO!

When The Bank Says No, The Economy Says No Too.

Okay, let’s apply your knowledge from the previous section here. When one bank says no to you personally, they won’t lend because you have poor credit. You were delinquent, you defaulted on your loans. Now what happens if banks says no to 50 million Americans for that same reason?

Well…. people use credit cards to purchase everyday goods and services

People gets a loan to purchase a car….

Finally, people use a loan TO GET A DEGREE IN COLLEGE!

In the case for Auto loans, if people are delinquent on their auto loans their car gets repossessed!

Speaking of repossessions, a report from Cox Automotive via Bankrate shows that almost 3.3 million vehicles was repo’d last year and 2023, compared to almost 2.5 million from 2020 and 2021… which according to the calculations is….

a 32% Increase and it’s getting worse by the day even to this year.

If you are delinquent on your credit card, you can’t finance your car or your mortgage, you need good credit!

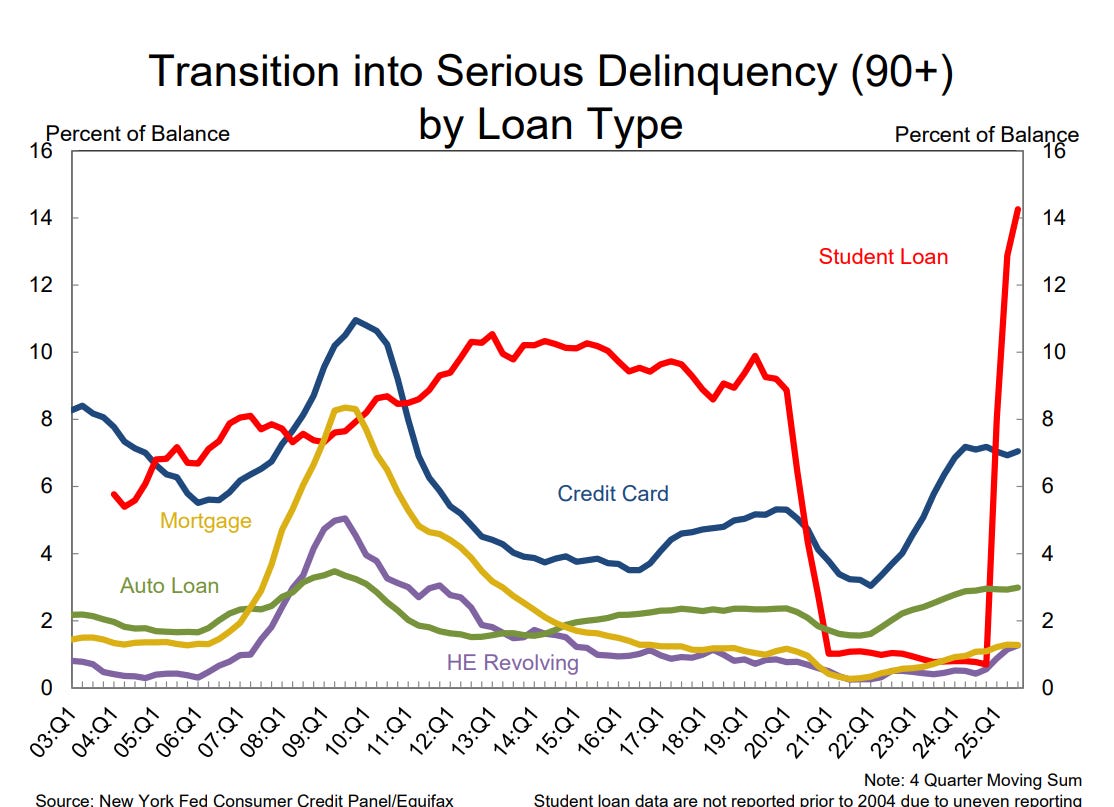

Same thing for student loans, which according to 3rd quarter report in the Household Debt and Credit Report from the Federal Reserve Bank of New York, Transition to serious delinquency, which is defined as 90 days or more past due soared to over 14% of balance, which is the highest EVER.

So, when people are delinquent, banks stop lending, money velocity, the rate at which money changes hands slows, Credit growth collapses due to banks lending less, that means there’s less spendable money in the system and all roads leads to a place that scares the living hell out of the rich:

DEFLATION.

That’s where everything is heading and there is nothing that any politician can do about it, domestically or globally, and the only way they can do to prevent deflation? By doing something that will make you, your family and your friend’s blood boil: